|

|

||||||

|

|

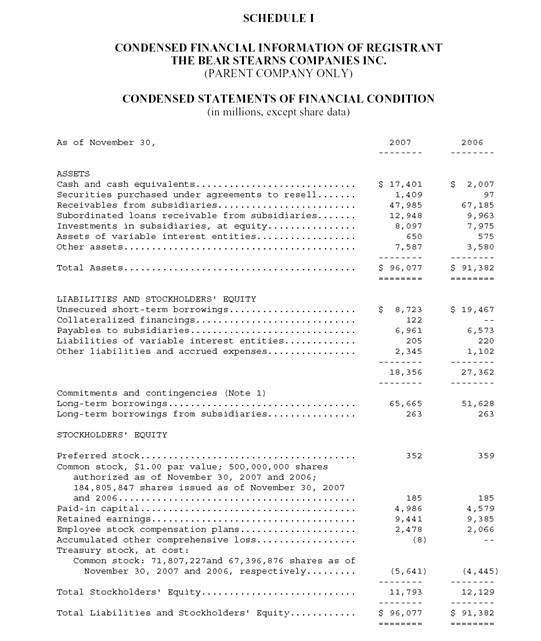

March 31, 2008 What Congress and Investors Should Understand About the Bear Stearns Deal Last week, both the House and Senate launched inquiries into the actions of the Treasury and Federal Reserve in committing public funds to J.P. Morgan's acquisition of Bear Stearns. It is important for Congress and the investing public to understand several features of this transaction: 1) The provision of a "non-recourse" loan is outside of the Fed's mandate under the Federal Reserve Act. Specifically, the Fed agreed to provide a $30 billion "non-recourse loan" to J.P. Morgan, secured only by the worst tranche of Bear Stearns' mortgage debt. This is not in fact a loan - if it were, J.P. Morgan would be required to pay it back, unless J.P. Morgan itself was to fail. Instead of a loan, this is a "put option," which protects J.P. Morgan from losses on the collateral, regardless of J.P. Morgan's own financial status. 2) The effect of the Fed's guarantee is not to protect the public, but to protect Bear Stearns' bondholders. By purchasing Bear Stearns, J.P. Morgan will take on the responsibility for paying off about $75 billion in claims to the short- and long-term bondholders of Bear Stearns. Yet J.P. Morgan requires only $30 billion from the Fed do this. This suggests that Bear Stearns' "book" of positions (excluding liabilities to Bear's own bondholders) would be worth at least $45 billion if transferred, netted, or otherwise settled. There is no reason that the public should take a loss at all. Rather, the book should indeed be sold to JPM or a competing acquirer, and the proceeds (probably far in excess of $45 billion) should be used to pay the senior claims of bondholders. Any excess over $75 billion would be a residual for stockholders. Simply put, the bondholders of Bear Stearns, not the public, should absorb any loss. 3) The deal is being defended on the notion that the global financial system would have "failed" had Bear Stearns not been rescued. But the orderly transfer, netting and settlement of financial derivatives and other "qualified financial contracts" (QFCs) is precisely what Title IX of the Bankruptcy Act of 2005 was written to facilitate. In effect, the Federal Reserve and the Treasury decided to ignore existing law and provide a bailout to the benefit of Bear Stearns' bondholders at public expense. 4) For Bear Stearns to "fail" means that it may not fully repay its own bondholders, but it has never meant that Bear Stearns' customers and counterparties would be hurt - their accounts and contracts are precisely what J.P. Morgan is eager to purchase and can easily transfer. The misuse of public funds is assisted by blurring the distinction between "failure" of Bear's customer and counterparty obligations (which nobody wants and is neither likely nor necessary), and the "failure" of Bear Stearns's stocks and bonds to be successful investments. Why should investment losses be bailed out at public expense? 5) The financial markets were relieved following the deal, despite a virtually complete loss of the company's stock value (over $20 billion in a matter of months). The risk of financial panic was not about potential losses to Bear Stearns' bondholders either. Instead, the market's relief focused on a single assurance: that J.P. Morgan stood behind the customer and counterparty obligations of Bear Stearns. Even if the Fed provides temporary liquidity, this assurance can still be achieved without a "non-recourse" feature, provided that Bear Stearns' bondholders are not defended against losses. 6) During the upcoming hearings, Congress can improve public confidence about the U.S. financial system by clarifying this distinction between "failure" of a company's obligations to customers, and the "failure" of a company's own securities. In most cases, the capital (stockholders equity and long term debt) of investment banks such as Bear Stearns is an adequate buffer, so that even in the event of bankruptcy, customer accounts and financial contracts can be quickly transferred to an acquirer, without ever exposing customers to losses. The public should understand that the bankruptcy provisions enacted in recent years expedite the transfer of these obligations, without an extended delay ("automatic stay"). The primary effects of bankruptcy are losses in the value of stocks and bonds issued by the failing company. 7) It appears likely that increased mortgage foreclosures will occur, and that stock prices may decline further, but actions like those of the Fed and Treasury will not avoid these outcomes. Rising foreclosures are the natural downside of a speculative housing boom financed by easy credit and suppressed mortgage rates. Protecting the bondholders of investment banks is not an efficient way to help homeowners. With regard to the equity markets, the rich valuations of recent years were largely based on historically high profit margins (due to a declining share of GDP being paid to workers as wages and salaries). The realignment of these profit margins, and of stock values, is largely inevitable, and is not something that the government should spend public funds to prevent. These uncomfortable realignments will probably continue for a while, but the U.S. economy will recover. 8) The clear historical role of the Federal Reserve has been to manage the composition of Federal liabilities (by varying the mix of Treasury securities and monetary base - currency and bank reserves - held by the public). The recent transaction is a dangerous break from that role, in which unelected bureaucrats are committing public funds to facilitate private business transactions and selectively defend the holders of corporate securities. Only Congress has the Constitutional right, by the representative will of the people, to commit public funds. The Bear Stearns deal is a dangerous precedent and a dilution of Congressional prerogative. Investors should not be in constant fear that the global financial system will "melt down" in the event of the bankruptcy of one large financial company or another. Though Bear Stearns apparently had the highest gross leverage (total assets to shareholder equity) among the large financials, and thereby provided a thin wall of defense for its stockholders, there was never a significant risk that the company would default on its obligations to customers and counterparties. Large U.S. financial companies are sufficiently well-capitalized that even in the event of outright bankruptcy, the only parties subject to loss are the stockholders and the bondholders of that particular company. The only instance in which this would not be the case is if the book value of the company was negative even after zeroing out all stockholder equity, long-term debt, and unsecured short-term debt. In short, investors should have confidence in the ability of the capital markets to function without the need for government bailouts at public expense. Below is a copy of Bear Stearns' balance sheet from the 10K filing in November. The largest financing (bondholder) items to note are the $8.7 billion in unsecured short-term borrowings and $65.7 billion in long-term debt. The Federal Reserve is protecting these from losses with public funds. Why?

Apart from a minuscule exposure to Bear Stearns through hedge positions in the S&P 500 Index, the Hussman Investment Trust has no long or short investment interests in Bear Stearns. The Fed moves to "sterilize" its term-lending intervention The misguided Bear Stearns intervention aside, the Federal Reserve does have a legitimate and essential role in providing short-term, fully-repayable funds (term repos and discount loans) to accommodate increased demand for liquidity in periods of crisis. But with the U.S. dollar weak, and inflation pressures still persistent, the Fed cannot simply "create money." Rather, the Fed is seeking to smooth the flow of transactions between liquidity-strapped and liquidity-rich segments of the economy, without causing an overall increase in the monetary base or the quantity of reserves in the banking system. Indeed, the Fed entered nearly $100 billion in open market operations in March. But these were not operations to buy Treasury securities and create more bank reserves. To the contrary, the Fed sold Treasury securities into the markets outright, and absorbed $100 billion from the financial sector. Why? The Fed did this to "sterilize" the increase in reserves caused by its "term securities lending" facility. (I should emphasize that this is something different than the Bear Stearns deal). Specifically, the Fed is accepting mortgage backed securities as collateral and providing temporary reserves to strapped financial institutions on one hand, but it is selling Treasury securities and reabsorbing those reserves from other participants in the financial markets who are seeking to hold safe, default-free assets. If the Fed did not do this, we would observe a surge in the quantity of the monetary base (currency and bank reserves), and most probably much stronger downward pressure on the U.S. dollar. Suffice it to say that by all evidence, the Fed is not on a rampage of "money creation," and is not just "running the printing presses." Instead, it is attempting to smooth the intermediation of mortgage securities, providing more time for the financial markets to rearrange the ownership of these from weak hands to stronger ones, while at the same time attempting to satisfy a voracious rush for safe havens such as Treasury securities. Those efforts at temporary liquidity provision represent smart, effective monetary policy. It is important to recognize the benefit of these actions, and they should indeed provide confidence to the financial markets. They will not provide solvency or substantially reduce the probable writedowns ahead, but they do benefit the markets by allowing increased liquidity and the ability for investors to flexibly alter their portfolios. Unfortunately, the ongoing provision of short-term liquidity by the Fed stands in strong contrast to the dangerous and misguided application of public funds in the Bear Stearns deal. That deal should be quickly busted and reorganized in a manner that assures that Bear's bondholders, not the public, carry the risk of loss. Bear Stearns did apparently overextend the amount of risk that its capital could absorb in a downturn, and by doing so, it put its own stockholders and bondholders at risk of loss. But I don't believe there was ever a risk of Bear "failing" on its obligations to customers and counterparties. If the participants in the financial markets don't quickly recognize the difference, they will undoubtedly create far more panic than is necessary. In the process, they will open the door for unelected bureaucrats to arbitrarily commit public funds in closed meetings; enriching and defending private parties in the name of "saving" the global financial system. Market Climate As of last week, the Market Climate for stocks remained characterized by unfavorable valuations and unfavorable market action on our measures, holding the Strategic Growth Fund to a fully-hedged investment stance. Though the stock market has rebounded somewhat from the oversold levels of a few weeks ago, conditions can't be considered "overbought" at present either. As I've frequently noted, about the only time I have pointed short-term views about near term direction is when stocks are overbought in an unfavorable Market Climate (a situation typically followed by steep losses) and when stocks are oversold in a favorable Market Climate (typically followed by strong recoveries). At present, we have neither, so while we are defensive based on the average return/risk profile that similar conditions have historically produced, I have no particular expectations regarding near-term direction. Generally speaking, it is true that the stock market has tended to bottom about 4-5 months before the end of a recession. It is quite dangerous, however, to assume that the current downturn in the market or the economy will be of a specific duration, and to start "looking for a bottom" on that basis. Just as market tops are marked by expectations that economic strength will persist indefinitely, stock markets hit bottom when an economic downturn is taken as full fact, when conditions are widely expected to get substantially worse, and when investors have largely given up on any hope that the economy will improve in the foreseeable future. My impression is that the early calls for a bottom ignore a realistic sense of history about how market peaks and troughs are formed. Once an ongoing and worsening recession is taken as a matter of common knowledge, it will be reasonable to talk about durable market lows. Until then, investors should recognize that a standard run-of-the-mill bear market averages a loss of about 30%. As usual, we are willing to accept a greater exposure to market risk on the basis of improved valuations or market action, but it is important to avoid the impulse to act without such evidence. Historically, bear markets that are associated with economic recessions tend to be deeper than those that occur without a recession. Moreover, as Tim Hayes of Ned Davis Research points out, cyclical bears that emerge in the context of a longer-term "secular" bear market also tend to be longer-than-average in duration: "Whereas the median cyclical bear has lasted about a year since 1900, the median duration has been 245 days during secular bulls and 525 days during secular bears. In other words, the revaluation process has tended to make cyclical bears last twice as long during secular bears." In bonds, the Market Climate remains characterized by unfavorably low yield levels and roughly neutral market action. Depressed yield levels reflect a very strong flight-to-safety here, and my impression is that long-term bonds do not have much investment merit (by the definition of yield-to-maturity, Treasury bonds are priced to deliver a long-term return of only about 3.5% annually over the next decade). As for speculative pressures, we did see another recession indicator fall into place, as aggregate weekly hours have now posted a quarterly decline. This adds to a broad list of other indicators that have typically been reliable signals of recession risk, well before economic downturns are taken as accepted fact. In precious metals, the Market Climate continues to be generally favorable, though we are likely to observe increasing volatility. Despite a relatively high gold/XAU ratio near 5.0, it is important to keep in mind that supporting trends in inflation and interest rates matter. At the point where CPI inflation begins to slow, and particularly if Treasury yields begin to rise, we would expect the weakness in the U.S. dollar to abate. At that point, we may observe a softening in commodity prices and the stocks of related companies. Suffice it to say that conditions are still favorable on our measures for now, but we are very conscious of the pressures on the U.S. dollar. As a rule-of-thumb, once we see Treasury yields higher than they were 6 months prior, inflation rates lower than 6 months prior, and the year-over-year CPI inflation rate below the 10-year Treasury yield, chances are that further gains in commodities will become more difficult. For now, the Strategic Total Return Fund has a constructive but not aggressive exposure of just over 15% of assets in precious metals shares. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |