|

|

||||||

|

|

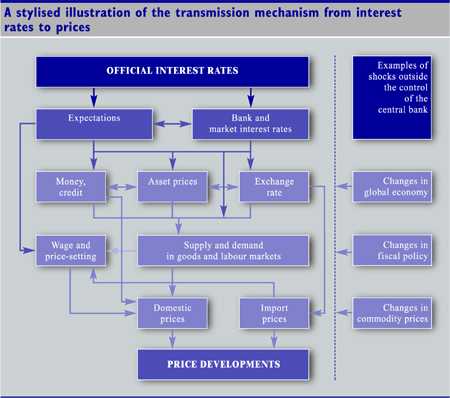

June 9, 2008 The Fed's Policy Rule: Regret-Minimax Well, that was a bit of a roller coaster. Last week, Ben Bernanke took a flier at "talking up the dollar," by suggesting that the Fed would eventually look to raise interest rates to support the buck. His remarks prompted a quick selloff in oil prices. The next day, Jean-Claude Trichet of the European Central Bank immediately called Bernanke's bluff by asserting that the ECB was poised to raise rates in attempts to contain inflation. The dollar plunged, and traders who were short oil were squeezed tightly, forcing oil prices up by $10.75 to over $138 a barrel. The unemployment figures didn't help, as the combination of mortgage problems and rising food and energy costs caused about 800,000 people to enter the labor force looking for, but not finding work. That surge in new entrants looking for work was what drove the unemployment rate up a full half-percent in a single month. While the surge in oil had the marks of a short squeeze, my own view continues to be that the commodities run will most likely complete its course during the coming quarter. As I noted a couple of weeks ago, "once a speculative price run-up becomes nearly vertical, it becomes very difficult to form expectations about the final price peak, since very small changes in the date of that peak imply significant differences in the final price. Still, the combination of a developing contango in the oil futures curve, a weakening global economy, and the likelihood of a moderate but positive supply response in the months ahead makes it unlikely that oil prices will escape their cyclical tendencies beyond the summer months." Dropping the transmission Wall Street commentary about the Fed typically assumes a great deal of certainty and presumed "knowledge" about how monetary policy affects the real economy: that it "works with a long and variable lag," that tighter monetary policy predictably reduces inflation, and that looser monetary policy increases lending and boosts the economy. But if you actually look at the data and work with it statistically, it's very difficult to prove any of that, and even more difficult to "connect the dots" between Fed actions and economic variables beyond those directly controlled by the Fed. Don't get me wrong. It's easy to demonstrate that the Fed predictably lowers rates in response to weaker economic indications, and that the Fed raises rates in response to indications of tight capacity and inflation pressures. The problem comes when you try to attach causality to what happens next - to demonstrate that a lower Fed Funds rate causes the economy to strengthen again, or to demonstrate that a higher Fed Funds rate causes inflation to dissipate, or to demonstrate that Fed interest rate changes or even changes in the volume of reserves are linked to the volume of bank lending. Fed-controlled interest rates typically follow, rather than lead, market-determined interest rates, and they add little incremental power in explaining economic and market fluctuations once market variables are taken into account. We can, of course, assume that the market interest rates are simply anticipating Fed moves, but there's no clear mechanism which the Fed Funds rate or reserve fluctuations can enforce changes in market interest rates. Why would we ever want to assume an unseen causal relationship with no observable mechanism, when that assumption adds scant explanatory power? Believing in the power of Fed actions is a lot like having the superstition that if you snap your fingers after the sun goes down, you will personally cause the sun to come up. The fact that the sun does, in fact, come up (though with a long and variable lag) isn't compelling evidence of causality unless you can identify the "transmission mechanism" linking the twitch of your fingers to the rotation of the earth. To offer some idea of how little even central bankers actually know about monetary policy, consider the following chart from the "Transmission Mechanism" page of the European Central Bank's website. The chart is intended to offer a "stylised illustration" of how the ECB's monetary policy actions might have an effect on inflation. Note that while "Official Interest Rates" are depicted in dark blue, indicating a high degree of certainty since they can be set directly, the shading immediately becomes lighter and lighter, indicating vague links and theoretical relationships. Somehow the "Price Developments" box at the bottom is given a hazy medium-blue shading, despite the fact that all roads to it are uncertain. But this is largely a matter of pride - it would be a bit odd for the ECB to depict even price developments in a very light shade of blue, because it would call the ECB's own effectiveness into question. Suffice it to say, however, that even central bankers have very little certainty about how their actions are predictably linked to anything.

My own view is that all of this focus on monetary policy misses the boat. Monetary policy is effectively subordinate to fiscal policy. No amount of monetary discipline can offset an undisciplined fiscal policy. The government budget constraint (Spending = Taxes + Treasury issuance to public + Increase in monetary base) is not a theory but an accounting identity. Moreover, since base money and Treasury debt are largely portfolio substitutes (and are priced to reflect identical marginal utilities), it turns out that government spending is a much stronger determinant of persistent inflation trends than money itself.

As you can see from the chart above, current inflation pressures are not surprising given the lack of fiscal discipline over the past several years (the persistent weakness in the U.S. dollar is no surprise either, and is likely to worsen). To reiterate my comments from September 10, 2007: "Inflation occurs when fiscal policy creates more government liabilities (either money or debt) than people are willing to hold at existing prices. If investors are scared about credit risks, they generally seek government liabilities as a safe haven, so you typically get deflationary pressure during credit crises. In contrast, if the government produces a lot of liabilities in an unproductive economy (as the Germans did in the 1920's, paying striking workers in the Ruhr even though they weren't producing anything), you get high inflation. It would not have mattered had Germany paid workers with bonds instead of money - bond prices would have declined, raising interest rates, lowering the willingness of people to hold non-interest-bearing currency, and causing a hyperinflation nonetheless. Inflation is first a fiscal phenomenon, tempered by economic activity and credit conditions, and affected only at the margin by "monetary policy." The government budget constraint (spending = taxes + debt + money creation) ensures that monetary policy cannot be independent of fiscal policy. All monetary policy does is to vary the mix of debt and money within that equation." As a side note, with all of that said, Senator Richard Shelby made an important observation last week that the Federal Reserve's intervention in the Bear Stearns' wipeout dangerously crossed the line from monetary policy to fiscal policy. I couldn't agree more. The Fed's actions in that case were outside of its mandate precisely because by taking Bear's assets into its own portfolio, the Fed effectively provided public funds to a private corporation without recourse if the collateral goes bad. Only Congress has that power. It was literally an illegal act, but it was also done so quickly that it was presented as an irreversible fait accompli. My impression is that there is less of a "Fed backstop" for other financial companies than investors believe, because the Fed is essentially on notice from Congress that the Bear deal went over the line. The Fed's Policy Rule: Regret-Minimax The essential fact is that even the policy makers themselves don't know the "true model" determining the course of economic growth, inflation, employment, exchange rates and other variables. When we recognize that central banks don't even have a clear idea about the "transmission mechanism" (if any) between their actions and their policy targets, it becomes easier to understand how they do set their policies. Suppose you are playing a game that involves both skill and chance. When you know the "true model" that ties your actions to some expected payoff, you can do all kinds of analysis, assess various probabilities, and then come up with the best action in a very principled, calculating way. But if you don't know the true model and you can't really predict the results of your actions, you're forced to move away from that sort of "Bayesian" analysis and instead make decisions that will be "robust" to even the worst-case scenario. In game theory, the choice that minimizes the maximum possible loss is called the "minimax" strategy. Suppose for example that you're Ben Bernanke, facing high inflation pressures but also enormous credit problems. We'll measure his payoffs in terms of circus peanuts. If the "true model" is that the credit problems are transient but the inflation problems are persistent, cutting rates will cause him to lose 5 peanuts, but raising them will cause him to lose just 1 peanut. On the other hand, if the "true model" is that the credit problems are on the edge of catastrophe, but the inflation problems are transitory, cutting rates will cause him to lose 4 peanuts, but raising them will cause him to lose 10 peanuts. So the maximum loss if he cuts rates is 5 peanuts (first model). The maximum loss if he raises rates is 10 peanuts (second model). If Bernanke doesn't know the true model, and doesn't even have a way of guessing the probability that one model or the other is right, then the "minimax" choice would be to cut rates. Let's go further and consider "regret." The worst regret from cutting rates would be if he cut and found out that the true model was actually the first one. In that case, he would have a "regret" of 4 peanuts (the 5 actually lost compared to just 1 that he would have lost if he raised rates). The worst regret from raising rates would be if he raised and found out that the true model was the second one, in which case, he would have a regret of 6 peanuts (the 10 actually lost compared with the 4 that he would have lost if he cut rates). In this case the "regret-minimax" strategy is to minimize the worst regret. Regret-minimax sometimes produces different choices than simple minimax, but in this case, Bernanke still chooses to cut rates. The apparent flip-flops and bad signals from Bernanke over the past year look like he is applying an inconsistent and changing set of principles, but in fact, it reflects his own "model uncertainty" and his choice to deal with that uncertainty by consistently applying a regret-minimax strategy. That's why he abruptly switched course from inflation fighting to desperate rate cutting over the past year. Despite clear inflation pressures, the Fed found itself repeatedly announcing "surprise" rate cuts, and raced to the rescue of Bear Stearns. Regardless of Bernanke's recent attempts to talk up the dollar, his adherence to regret-minimax is also why the Fed will find itself creating more surprise "liquidity facilities" in the coming months to address fresh credit problems. It's possible that we'll even see another large surprise rate cut on some morning that looks like the markets may open weak, but his preference will lean toward announcing ever more novel credit facilities while trying to avoid driving the dollar into a tailspin. Policy makers at the Fed know nothing more than anybody else about how mortgage problems, and credit problems, and commodity price pressures, and dollar weakness will affect the real economy, or even how its own actions will affect those outcomes, so the Fed has simply chosen (and will continue to choose) the course of action that will minimize regret in the worst-case scenario. Indeed, the only point we'll see the Fed actually raising rates in the coming year or so is if the apparent payoffs shift so much that failing to raise rates will appear costly and potentially regrettable to the Fed. We're nowhere close to that, and most probably won't be until we observe either an extended improvement in the employment picture (which would prompt rate hikes in hopes of stemming demand, speculation and excessive lending), or a dollar crisis (which would prompt rate hikes in attempts to stem the losses). Again, my own view is that the "true model" is one where the Fed has an important role in providing temporary liquidity to satisfy spikes in the demand for currency during a credit crisis, where the Fed can certainly have an effect when it operates outside of its charter (as it did in the Bear Stearns transaction), but where Fed policy otherwise has very little impact aside from market psychology. Still, to the extent that this psychology is important, particularly in the short-run, it is probably best to assume that Fed actions will be dominated by the regret-minimax criterion of doing whatever will produce the least regret in the worst case scenario. It's difficult to envision the payoffs tipping in favor of raising rates or tightening policy anytime soon. As for the European Central Bank, the mandate of the ECB is strictly on price stability (given Europe's experience with destabilizing inflation, concerns about that are deeply entrenched). As a result, the ECB tends to implement policy under the constant assumption that inflation, when it emerges, will be very persistent. This will lend a tightening bias to the ECB until commodity prices begin to weaken, most likely later this summer, and evidence of economic weakness becomes compelling enough to take recession as a reality rather than a subject of debate. The combined result is that we can probably expect further pressure on the U.S. dollar, and Fed policy that will continue to lean toward easing as fruitlessly as it did throughout the 2000-2002 downturn. Market Climate As of last week, the Market Climate for stocks was characterized by unfavorable valuations and unfavorable market action. The stock market has made a few attempts in recent weeks at recruiting some speculative momentum, but those attempts have tended to fail abruptly. If we do observe a more compelling improvement in market internals, suggesting that investors' aversion to risk has subsided, I would expect to cover a portion of the short-call option side of our hedges. For now, the Strategic Growth Fund remains fully hedged. In bonds, my inclination is to expect some downward pressure on yields as economic signals deteriorate. There is a good deal of "headline pressure" from the spike in unemployment, rising oil prices, and weak housing. All of these are likely to reinforce some retrenchment among consumers, which could help to tip the U.S. economy more definitively into recession. Still, the prospect of 10-year total returns of just 4% in Treasury bonds is not particularly compelling on an investment basis, so the primary driver of bond returns will be speculation about economic weakness and a "flight to safety" from credit concerns. If we observe somewhat higher yields in Treasuries, we'll be inclined to extend our maturities somewhat, but here, our overall duration in the Strategic Total Return Fund remains less than one year. The Fund continues to hold about 15% of assets in foreign currencies as well. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |