|

|

||||||

|

|

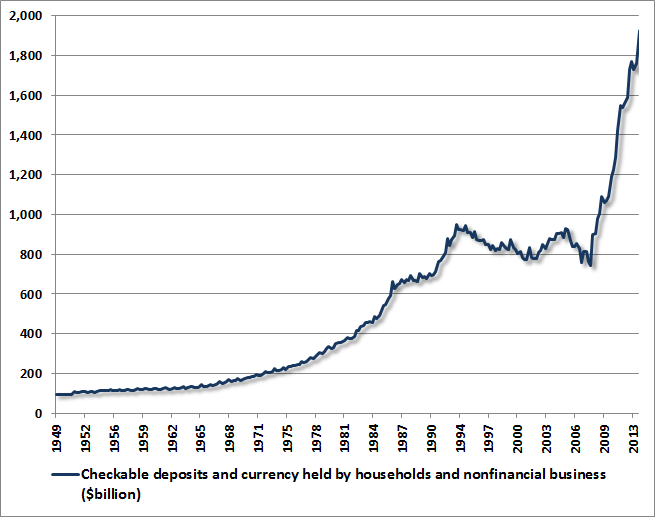

March 17, 2014 Restoring the "Virtuous Cycle" of Economic Growth During the past 14-year period, the S&P 500 has achieved a total return, including dividends, of just 3.3% annually. Even this outcome has been achieved only because market valuations have now been driven more than 100% above pre-bubble historical norms, based on reliable measures that are highly correlated with subsequent market returns (for a review, see It is Informed Optimism to Wait for the Rain). We emphasize reliability because there are countless measures that Wall Street analysts prefer to use, particularly those that make stocks seem reasonably valued. The problem is that most have very little relationship with actual subsequent market returns. When evaluating anyone’s valuation claim, you should always ask – how does this measure actually relate to subsequent market returns when it is evaluated over decades of market history? Over the same 14-year period, real U.S. GDP has grown by just 1.8% annually, while real gross private investment has crawled at just 1% annually. The primary growth area of the economy has been total public debt, which has surged at 8% annually, driving the outstanding amount of total public debt to 99% of GDP. Of course, the Federal Reserve has absorbed trillions of this debt, which has allowed federal debt held by the public to stay closer to 70% of GDP. As the Fed buys that debt, it pays for it by creating currency and bank reserves (monetary base) that must be held by someone in the economy at each point in time. In aggregate, this cash doesn’t represent an untapped economic resource that is waiting to be deployed, but is instead a receipt for economic resources that have already been deployed. The cash held by any individual (over and above debt that is owed) is simply evidence that at some point in the past, they consumed less than the full value of their own output, so that someone else could consume more than the value of their own output. In the future, these IOUs can be used to claim new production at some point in time (which does not have to be immediate), allowing the holders to consume more output than they produce, but only by requiring others to consume less output than they produce. In short, all of this cash does not represent aggregate wealth. Instead, it is a placeholder that determines how future production will be allocated. Now, one might wish that the abundance of these IOUs of past economic activity would immediately translate into efforts to deploy them into future economic activity. Unfortunately, as F.F. Wiley demonstrated last week (h/t ZeroHedge), there is no relationship between corporate cash and subsequent capital expenditure, nor is the level of capital expenditure even well-correlated with the level of real interest rates. Quantitative Easing and “Cash on the Sidelines” The Federal Reserve’s policy of quantitative easing has certainly had a massive effect on the form of the IOUs held by individuals and businesses. Following the massive government deficits of recent years, one would expect that the IOUs would be held as Treasury securities. But the Fed has bought trillions of dollars of that debt, and replaced it with currency and bank reserves. Regardless, holding the IOUs in the form of cash does little to provoke individuals or businesses to spend them. What the Fed’s policy has done, however, is to encourage investors to reach for yield in speculative assets in the hope of greater returns than are available on zero-interest cash. Where does all this cash “go”? In aggregate, equilibrium ensures one precise answer: nowhere. Though any individual can get rid of their cash by buying stocks or other risky assets, the seller of those same assets then gets the cash. It doesn’t vanish, it only changes hands. Once a government liability is created, its form may change between Treasury debt, currency and bank reserves, depending on what the Fed does, but that liability will continue to exist in one form or another until the government runs a surplus and retires the liability from circulation. Meanwhile, the existing cash simply creates an ongoing game of “hot potato” from one holder to another. The effect of QE has been to make this potato very hot, encouraging investors to chase one risky security after another, so that now nearly every risky asset has been driven to such rich valuations that their probable future returns match the zero return available on cash. Over the short-term, driving risky assets to valuations associated with zero future returns may be an equilibrium in a world where cash presents the same dismal opportunity. But this is also a highly unstable equilibrium. A broad range of historically reliable valuation metrics now imply zero or negative expected nominal total returns on the S&P 500 – with the additional likelihood of deep intervening losses – over every horizon shorter than about 7 years. Over a full decade, we estimate 10-year nominal total returns for the S&P 500 averaging just 2.4% annually. In 2007, I noted that investors were likely to observe a growing amount of what would wrongly be viewed as “cash on the sidelines,” for the simple reason that the government was likely to run massive deficits and someone would be left holding the resulting IOUs. The commercial paper market had also dried up, suggesting that companies would likely rely on bank finance to a greater extent. Since then, we’ve indeed observed massive deficits and a shift in the composition of corporate finance, but the composition of short-term liquidity has taken an interesting form. At the government level, what would have been a mountain of new Treasury securities has been transformed by the Fed into a mountain of currency and bank reserves. At the corporate level, QE has caused a “reach for yield” that has enabled corporations to issue cheap intermediate-term (3-7 year) debt. The proceeds of that debt are being largely held as cash, and have essentially substituted for the availability of working capital through the commercial paper market, without relying heavily on bank credit. To illustrate the effect of the Federal Reserve’s conversion of various IOUs (Treasury and mortgage debt securities) to the form of currency and bank reserves, the chart below shows the aggregate amount of currency and checkable deposits (nearly $2 trillion) now held by households and businesses. Note the upward ramp since the Fed initiated its policy of quantitative easing. The sheer dollar amounts are constantly used to argue that this “cash on the sidelines” is on the verge of being “deployed” by moving it "into" equities, capital goods, and so forth. But remember, the liquidity created by the Fed in recent years is a “hot potato” – someone in the economy must hold it at every point in time. It is created by the Fed as a replacement for mortgage securities and Treasury debt, and must be held by someone in lieu of other stores of value. In aggregate, the cash balances are held by corporations in an amount that doesn’t even cover their own new debt issuance in recent years. Moreover, there is zero relationship between such cash balances and subsequent capital expenditure. What you are looking at is simply a mountain of IOUs based on past economic activity. The thing that matters for future activity is whether there are productive and desired opportunities to bring new goods and services into existence.

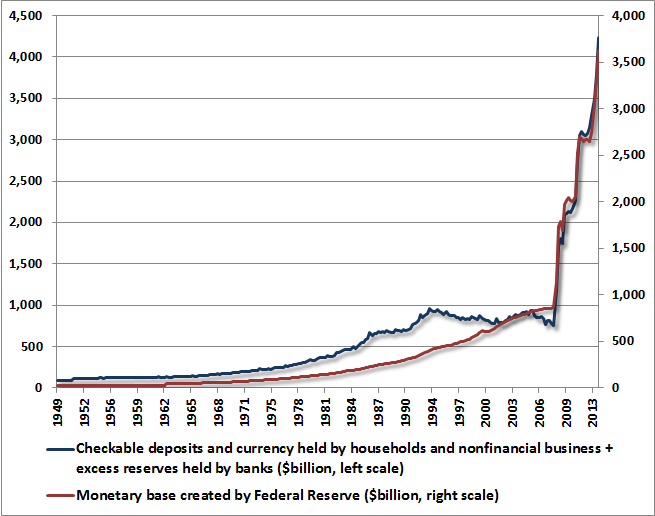

In case there is any doubt that the currency and reserves created by the Federal Reserve must be held by someone in the economy at each point in time, the chart below combines deposits and currency held by households and non-financial business with the excess reserves held by the U.S. banking system [Geek's Note: there is some overlap between deposits and reserves here, but the central point should be obvious]. This is what quantitative easing has wrought. None of this liquidity is any more likely to be spent simply because the IOUs are in the form of currency and reserves instead of earning assets. The imbalance of IOUs has simply resulted in the severe overvaluation of other asset markets. Again, what matters for a spending decision is whether there are productive and desired opportunities to pursue new economic activity now – and that question depends entirely on the extent to which the U.S. economy can escape from more than a decade of speculative, unproductive, Fed-induced resource misallocation.

Restoring the “Virtuous Cycle” of Economic Growth At this point, it should be clear that the mere existence of a mountain of IOUs related to past economic activity is not enough to provoke future economic activity. What matters instead is the same thing that always matters: Are the resources of the economy being directed toward productive uses that satisfy the needs of others? To the extent that such desirable activities exist – whether as consumption goods or as investment goods like machines, the act of bringing them forward not only engages existing resources (such as factory capacity and labor), but also creates new income that can be used to purchase yet other desirable products. This is what creates a virtuous circle of economic activity and growth. Not quantitative easing, not suppressed interest rates, not speculation. The resources of the economy must be channeled toward activities that are actually productive, desirable, and useful to others. When this doesn’t occur – when companies produce output that isn’t wanted, when capital investments are made that aren’t productive, when housing is constructed at a pace that exceeds the sustainable demand and ability to finance it – the act of production and the resources of the economy are wasted. That is really the narrative of the past 14 years, and is largely the result of repeated bouts of Fed-induced speculation and misallocation. Robert Blumenthal recently wrote an excellent essay describing the economic costs of such “malinvestment.” At the moment that a person uses their labor to produce something of value to others, that person’s own income is enhanced, and the ability to purchase the output of others is also created. As economist Jean-Baptiste Say wrote, “A product is no sooner created than it, from that instant, affords a market for other products to the full extent of its own value... Thus the mere circumstance of creation of one product immediately opens a vent for other products.” In a healthy economy, the productive activity of one sector opens a vent for the productive activity of other sectors of the economy. The useful allocation of resources in one area of the economy reinforces the useful allocation of resources in another. Economic growth continues as the efforts of each sector focus on the production of those things that will be of demand and use to others. Each productive act is not simply an event, but contributes momentum to a virtuous cycle. The difficulty emerges when something is brought into production that is not desired – that fails to align with the actual demand for it. In that event, the value of the product itself may be less than the value of the resources committed to its production. Since it is not consumed, it simultaneously becomes “savings” and “unwanted inventory investment.” Long-term growth is harmed, because economic effort and resources are wasted and fail to open a vent for other production. If this occurs at a large scale, jobs are lost, inventories build, and the economy suffers the long-term effects of misallocated activity. When we review the economic narrative of the past 14 years, this is exactly what we observe. The first insult occurred during the excesses of the tech bubble and the severe misallocation of capital that resulted. Next, in response to the economic downturn in 2000-2002, the Federal Reserve held interest rates down in the hope of reviving interest-sensitive spending and investment. Instead, the suppressed interest rate environment triggered a “reach for yield” that found itself concentrated in enormous demand for mortgage securities. Wall Street was more than happy to provide the desired “product,” but could do so only by creating new mortgages by lending to anyone with a pulse. The resulting housing bubble became a second episode of severe capital misallocation, and led to the economic collapse of 2008-2009. In response to that episode, the Federal Reserve has now produced and largely completed a third phase of speculative malinvestment, this time focused on the equity market. On historically reliable valuation measures, equity prices are now double the level at which they would be likely to provide historically normal returns. As in 2000, three-quarters of the record new issuance of equities is now dominated by companies that have no earnings. The valuation of the median stock is now higher than it was at the 2000 peak. NYSE margin debt as a percent of GDP exceeds every point in history except the March 2000 peak. All of this will end badly for the equity market, but the real insult is what this constant malinvestment has done to the long-term prospects for U.S. economic growth and employment. The so-called “dual mandate” of the Federal Reserve does not ask the Fed to manage short-run or even cyclical fluctuations in the economy. Instead – whether one believes that the goals of that mandate are achievable or not – it asks the Fed to “maintain long run growth of the monetary and credit aggregates commensurate with the economy's long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates.” What the Fed has done instead is to completely lose control of the growth of monetary aggregates, in an effort to offset short-run, cyclical fluctuations in the economy, so as to promote maximum speculative activity and repeated bouts of resource misallocation, and ultimately damage the economy’s long-run potential to increase production and promote employment. In the face of our concerns about long-run consequences, some might immediately appeal to Keynes, who trivialized prudence and restraint, saying “In the long run, we are all dead.” But we are not talking about decades. The insults to the U.S. economy, to U.S. labor force participation, and to the long-term unemployed are the largely predictable result of policies that have been pursued in the past decade alone. On the fiscal policy side, there are numerous initiatives that – when properly focused on productivity and labor force participation – could easily be self-financing for the economy in aggregate. Too much of our fiscal deficit has nothing to do with productivity or inducements that reward economic activity. Productive infrastructure (ideally projects that have large distributed effects, as opposed to notions like rural broadband), alternative energy, earned income tax credits, tying extended unemployment compensation to some sort of activity requirement (community, internship or otherwise), small business loans and tax credits tied to job creation and retention, investment and R&D credits, and other initiatives fall into this category. The objective is for the private markets to retain a vested interest and exposure to some amount of risk, so that losses and unproductive decisions remain costly, but also for fiscal initiatives to ease constraints that are binding on private decision-making. On the monetary policy side, it’s simply time to change course to a far less "elastic," rules-based policy. With $2.5 trillion in excess reserves within the banking system, even one more dollar of quantitative easing is harmful because it perpetuates financial distortion and speculative activity while doing nothing to ease any constraint in the economy that is actually binding. Fortunately, it actually appears that the FOMC increasingly recognizes this, as attention has gradually focused on questions about policy effectiveness and financial risk, and away from the weak hope for positive effects. We will have to see how long this insight persists, but statements from FOMC officials increasingly reflect the intention to “wind down” QE, and emphasize the “high bar” that would be required to move away from that stance. The cyclical risk for the U.S. equity market is already baked in the cake, and we view downside potential as substantial. The economy would allocate capital better, and to greater long-term benefit, if interest rates were at levels that rewarded savings and discouraged untethered growth in fiscal deficits. The economy would also allocate capital better if equity valuations were closer to historical norms (unfortunately about half of present levels given the extent of present distortions). While the capital markets are likely to undergo a great deal of adjustment in the coming years, we don’t anticipate systemic economic risks similar to the 2007-2009 period. We do observe a buildup of inventories in recent quarters that, combined with disruptions abroad, seem likely to contribute to economic weakness, but there are numerous episodes in history when stock market losses were not associated with steep economic losses. The largest economic risks are particularly likely to emerge in Asia, where “big bazooka” central bank policies and speculative overinvestment have also produced large and persistent misallocation. China and Japan are of principal concern, though many smaller developing countries outside of Asia also appear at risk. Policy makers should certainly focus on areas where exposure to foreign obligations, equity leverage, and credit default swaps would produce sizeable disruptions. In any event, I believe it is urgent for investors to recognize the current position of the U.S. equity market in the context of a complete market cycle. As I noted in the face of similar conditions in 2007, my expectation is that any “put option” still provided by the Federal Reserve has a strike price that is way out-of-the-money. The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Only comments in the Fund Notes section relate specifically to the Hussman Funds and the investment positions of the Funds. Fund Notes The Hussman Funds continue to adhere to a defensive stance toward equities and a moderately constructive stance toward Treasury bonds and precious metals shares. As usual, we expect these positions to shift as market conditions change. In particular, we encourage shareholders to review our remarks in last week’s market comment. As I’ve written many times, the assumption that we have a permanently defensive stance toward the equity market is an artifact of our 2009-2010 stress-testing period, which prevented a bullish interval between our defensiveness in the 2007-2009 decline, and our recent defensiveness (in response to market conditions that have historically had wickedly negative outcomes). It should be clear – both from our commentary at that time and from our valuation methods – that our concern was not market valuation (our estimates of 10-year prospective S&P 500 returns in late-2008 and 2009 were in the 10-12% annual range) but rather the ability to distinguish between a “post-war” and “Depression-era” state of the world. In the Depression, valuations similar to those of early-2009 were followed by further losses that erased another two-thirds of the market’s value, and numerous measures of market action (including many that were effective in post-war data) were badly whipsawed. Ensuring that our methods were robust to that “two data sets” problem is something I still view as an appropriate fiduciary response, but the 2009-2010 miss also produced a “permabear” reputation that we wholly reject. We expect that the completion of the present cycle and the course of the next will encourage the full range of market exposures contemplated by our investment discipline – from strongly defensive as we are at present, to fully unhedged and, in Strategic Growth Fund, even leveraged using a small percentage of assets in index call options. Our strongest return/risk estimates generally emerge when a material retreat in valuations is followed by an early improvement in our measures of market action. If a shift to a largely or fully unhedged stance under such conditions would be surprising or unanticipated, we urge shareholders to review our Prospectus and annual reports. It is in everyone’s interest to ensure that our shareholders have a strong understanding of the Funds and their investment strategies. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |

{kind=link}