|

|

||||||

|

|

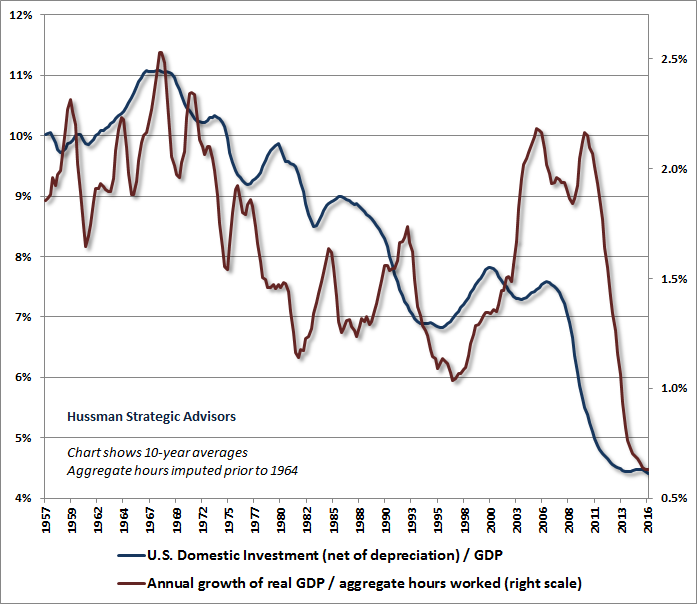

November 21, 2016 Action and Reaction “My advice would be that several principles should be taken into account as you make these judgments. First of all, the economy is operating relatively close to full employment at this point, so in contrast to where the economy was after the financial crisis, when a large demand boost was needed to lower unemployment, we’re no longer in that state. CBO’s assessment is that there are longer-term fiscal challenges; that the debt/GDP ratio at this point looks likely to rise as the baby boomers retire and population aging occurs; and that longer-run deficit problem needs to be kept in mind. In addition with the debt/GDP ratio at around 77%, there’s not a lot of fiscal space should a shock to the economy occur; an adverse shock that did require fiscal stimulus. “I think what’s been very disappointing about the economy’s performance since the financial crisis, or maybe going back before that, is that the pace of productivity growth has been exceptionally slow: the last 5 years, a half percent per year; the last decade, one and a quarter percent per year. The previous two decades before that were about a percentage point higher, and that’s what ultimately determines the pace of improvement in living standards. So my advice would be as you consider fiscal policies, to keep in mind and look carefully at the impact those policies are likely to have on the economy’s productive capacity, on productivity growth, and to the maximum extent possible, choose policies that would improve that long-run growth and productivity outlook.” Janet Yellen, 11/17/16 testimony to the Joint Economic Committee I have to say that of all of Janet Yellen’s discussions since taking the position of Fed Chair, last week’s comments to the Joint Economic Committee struck me as the most lucid. Perhaps it’s only because they align with my own economic views on the critical role of productive investment (see last week’s comment Judging Economic Policy), but it also appears that since the Fed is now on a course of slow normalization of monetary policy, Yellen has less need to justify the continuation of a reckless policy on the basis of empirically unsupported arguments. The slow growth in productivity noted by Yellen has been paced by weakness in U.S. real gross domestic investment. We’ve actually observed zero growth in U.S. real gross domestic investment over the past decade, compared with growth of about 4.5% in the half-century prior to 2000. The chart below expands on the one I presented last week, showing U.S. domestic investment (after depreciation) as a share of GDP, compared with the growth in real output per labor hour.

While the markets appear convinced that substantial infrastructure spending is forthcoming, the existing policy discussions remain quite vague, and the focus strikes me as all wrong. As other observers have correctly emphasized, the U.S. lacks enough skilled labor in the heavy construction sector to actually implement large-scale infrastructure spending projects on the scale being discussed, unless foreign firms were recruited to implement them. As for energy-related projects, my impression is that sucking the last vestiges of fossil-stored sunlight out of the ground using more technically-advanced straws is less of an investment than a reflection of stunted vision, given that unlimited amounts of convertible sunlight are, and will be, available as long as humanity exists. Not that a Republican-led Congress that leans to the fiscally conservative side would be likely to approve massive new spending in any of these areas, but even if it did, the first dollar would not likely be spent until well into 2018. Meanwhile, though it’s widely suggested that repatriating corporate cash held abroad would lead to a huge expansion of new investment, this idea runs into two problems. First, major corporations already have ample access to funding for any project they could reasonably consider. Even if cash is held overseas, it’s rather easy for corporations to effect interest-rate swap transactions that effectively make the funds available domestically (invest cash held abroad to receive floating-rate interest, borrow funds domestically and pay a fixed rate, enter an interest-rate swap that pays floating and receives fixed, and it’s as if you’ve instantly brought your money home). Moreover, providing tax breaks to corporations to repatriate funds is nothing new. The U.S. did the same thing in 2004. Rather than creating jobs, the funds were largely used for corporate stock buybacks, acquisitions, dividends and bonuses, while the top corporate beneficiaries actually cut jobs and decreased research spending. So let’s encourage productive investment, particularly where those investments relieve binding economic constraints, expand capacity in useful and sustainable directions, carry spillover benefits for others in the economy, require those who use public funds to have their own capital also at risk, and are likely to produce substantial economic benefits per dollar spent. But let’s not squander a great opportunity for a pro-investment fiscal agenda by imagining that the economy will benefit from massive loosely-conceived infrastructure projects or tax breaks that rely on misleading economic and financial arguments for their public support. Over the past couple of weeks, the financial markets have been jostled by wide dispersion across economic sectors and security types based on thin evidence about potential economic policies. My sense is that investors are exuberant to have a new theme, any theme, other than watching the Federal Reserve. From a monetary policy front, my view remains that the primary effect of Fed policy in recent years has been to encourage speculative yield-seeking. My own argument in favor of normalizing policy is not that the economy is “overheating” or that inflation is a risk, but primarily that deviations from systematic policy have no economic benefit and impose substantial costs on the economy over horizons that are longer than the Fed seems to contemplate (see Failed Transmission: Evidence on the Futility of Activist Fed Policy for detailed evidence on this point). That said, I do think it’s worth noting that even if CPI inflation was to run at an underlying rate of 2% in the coming months, the year-over-year inflation rate in the CPI will hit 2.4% by February, and 2.5% by March, simply as a result of how the existing CPI figures work. As for the post-election theme-chasing, we observe that across many asset classes, reliable measures of investor sentiment have been driven to extremes of optimism (equities, the U.S. dollar) and pessimism (bonds, foreign currencies). Within equity market action, we also see wide internal dispersion, which remains consistent with underlying risk-aversion among investors, at valuations that remain obscene from a historical perspective. While we're hearing historically uninformed references to the extended bull markets of the 1980's and the 1950's, the most reliable market valuation measures are presently over four times their 1950 and 1982 levels. The effect of politics on full-cycle and 10-12 year market outcomes is negligible, compared with the impact of valuations. Over shorter segments of the market cycle, election results do have the capacity to affect investor sentiment (particularly preferences toward risk), so a focus on the quality of market action will remain important. Near-term, my impression is that much of the recent market response is overdone, and that the markets are vulnerable to decided reversals in the opposite direction of recent trends. As I noted last week, extreme valuations already establish the likelihood of near-zero 10-12 year S&P 500 total returns, and a 40-55% market decline over the completion of the current cycle. The extended speculation in the recent half-cycle was rooted in monetary distortion and risk-seeking that is now unwinding, and we continue to expect the completion of this cycle within the natural course of action and reaction. As for the near-term market return/risk classification, last week’s shift toward increased internal dispersion and greater equity market bullishness shifted our estimated market return/risk classification from a relatively neutral outlook back to hard-negative. That will change as valuations, market internals, and other factors do, and we’ll align our outlook with new evidence as it comes. On the economic front, the overall profile of coincident and leading measures remains consistent with a low-level churn, not far from levels that have historically been associated with recessions, but not yet breaking down to levels that would raise immediate concerns. I’ve always emphasized that recessions are periods where the mix of goods and services demanded by the economy becomes misaligned with the mix of goods and services currently being supplied. In this context, high inventory/sales ratios, flat-lining year-over-year real growth rates, and expanding dispersion in the financial markets between various sectors and security types strikes me as a warning sign rather than a sign of optimism for the U.S. economy. Again, there will be little fiscal spending impact until 2018. To the extent that any is coming, it will exert its effect over time, while financial conditions will have a more rapid effect. Rather than focusing on sectors such as banks, infrastructure, pharma, and transports, my impression is that investors should be watching the bond markets, particularly if corporate and low-grade bonds join or exceed the deterioration in Treasury debt. A final comment. I’ve long believed that if we are incapable of having peace in ourselves, we will be incapable of having peace in the world. I think that’s true on every side, but because it’s possible to appeal to both the best and worst in humanity, I also believe that leadership matters. As we discover the cabinet members and nominees who may comprise our next administration, we should be attentive to whether they reflect character and peace in their countenance, words and actions. Great leaders are remembered as those who call, as Lincoln did in his first inaugural address, on the “better angels of our nature.” They don’t wait for others to do the same, but instead lead by example. All of us have the choice to listen to those better angels of our nature, or to instead be seduced by appeals to the worst elements within us. History records how long it takes us to choose well. Both in domestic and international conflicts, it’s possible to recognize our shared humanity, and to address the concerns, perceptions and even suffering of each other, in ways that are consistent with our own security and legitimate interests, but without adopting the language of “enemy.” Much of the distress of our nation and our world has been the result of needless war, of injustice, of incivility, and of financial greed masquerading as economic promise. If we aren’t discerning, we will have respite from none of it.The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Please see periodic remarks on the Fund Notes and Commentary page for discussion relating specifically to the Hussman Funds and the investment positions of the Funds. --- The foregoing comments represent the general investment analysis and economic views of the Advisor, and are provided solely for the purpose of information, instruction and discourse. Prospectuses for the Hussman Strategic Growth Fund, the Hussman Strategic Total Return Fund, the Hussman Strategic International Fund, and the Hussman Strategic Dividend Value Fund, as well as Fund reports and other information, are available by clicking "The Funds" menu button from any page of this website. |

|||||||||||||||||||||||||

|

For more information about investing in the Hussman Funds, please call us at

1-800-HUSSMAN (1-800-487-7626) 513-326-3551 outside the United States Site and site contents © copyright Hussman Funds. Brief quotations including attribution and a direct link to this site (www.hussmanfunds.com) are authorized. All other rights reserved and actively enforced. Extensive or unattributed reproduction of text or research findings are violations of copyright law. Site design by 1WebsiteDesigners. |